Posting to the general ledger is the step accounting materials love to skip. You learn debits on the left, credits on the right, and then the textbook jumps ahead with a quick instruction to “post it to the ledger.” That shortcut hides an important part of the accounting process — and it’s why posting stays vague for so many students and new accountants.

This post walks through exactly what posting means, how it works step by step, and why it matters, with two worked examples showing how running balances actually update.

What Does Posting to the General Ledger Mean?

Posting to the general ledger means transferring each line of a journal entry into the specific account it affects, where it updates that account’s running balance. Creating journal entries comes first; posting journal entries to the ledger is the step that follows. A journal entry records one complete transaction, but every debit and credit line within it is posted to its own account in the ledger.

In other words, a journal entry does not sit in one isolated place. Each row flows into the proper account, becomes part of that account’s history, and updates its running balance.

This is double entry bookkeeping at work. Every transaction affects at least two accounts, total debits always equal total credits, and the accounting equation — assets equal liabilities plus equity stays in balance after every posting.

What Is a General Ledger?

The general ledger is the complete record of a company’s accounts and the financial activity posted to those accounts. It is the central place where transactions are organized by account, balances are updated, and the numbers that eventually support the trial balance and financial statements begin to take shape.

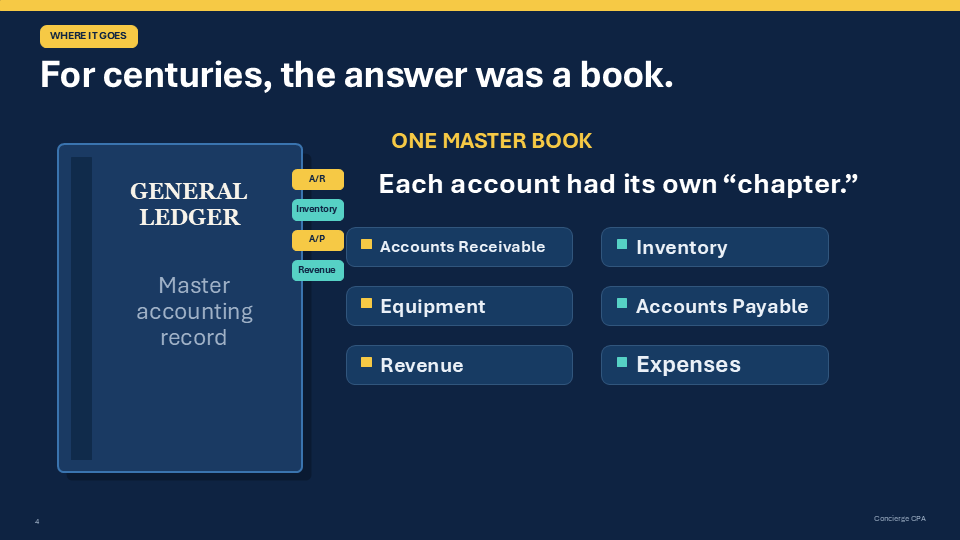

For centuries, the general ledger was literally a book. It was the master accounting book, and each account had its own section. You could think of it like a book with chapters for accounts receivable, inventory, equipment, accounts payable, revenue, rent expense, and every other account the business used.

Each section gathered every transaction that affected that account and kept a running balance. That basic idea has not changed at all. The only real difference is the format.

Today, the general ledger usually lives inside accounting software instead of a physical book. Whether a company uses QuickBooks, NetSuite, Oracle, Workday, or another system, the accounting structure is still the same. The book may be gone, but the logic is still there.

How to Post Journal Entries to the General Ledger (4 Steps)

Posting to the general ledger follows a simple pattern:

- Record the journal entry. The transaction is first captured in the journal with the transaction date, the account names affected, and equal debit and credit amounts.

- Identify each account named in the entry. Every line of the entry belongs to a specific general ledger account.

- Post each debit or credit line to that account. The lines are split apart — each one goes to its own account in the ledger.

- Update the running balance in each affected account. The new posting changes where that account stands.

That’s the whole mechanism. Now let’s watch it happen with real numbers.

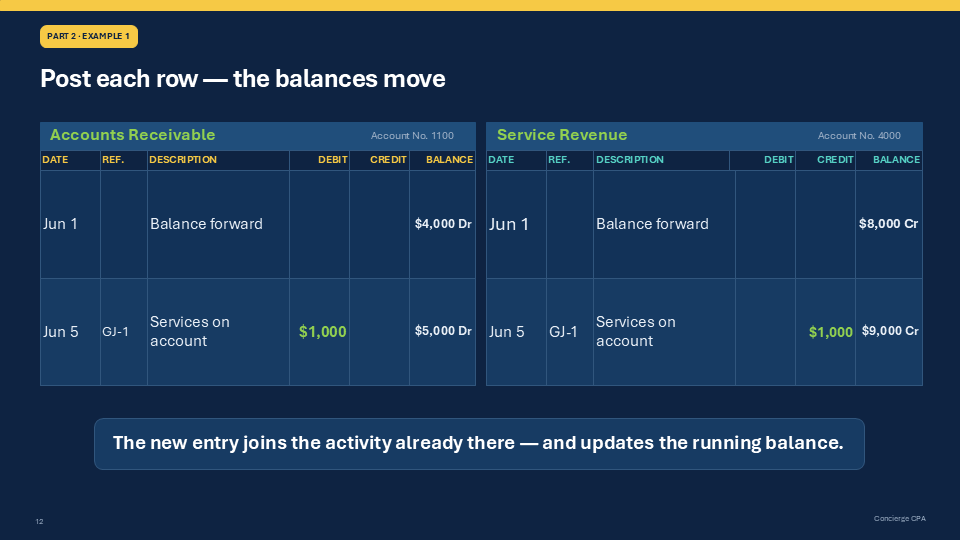

Example 1: Posting a Sale on Account

Assume a business provides services worth $1,000 to a customer and allows payment later.

The journal entry would be:

- Debit accounts receivable for $1,000

- Credit service revenue for $1,000

Now look at what happens in the general ledger.

Accounts Receivable

The $1,000 debit is posted to the accounts receivable account.

If that account already had a debit balance of $4,000 from earlier credit sales, the new posting raises the balance to $5,000.

Service Revenue

The $1,000 credit is posted to the service revenue account.

If service revenue already had a credit balance of $8,000, the new posting increases it to $9,000.

This is the key point: the journal entry does not create separate floating pieces of information. Each part of the transaction is absorbed into the proper account in the general ledger, and each account’s balance is updated.

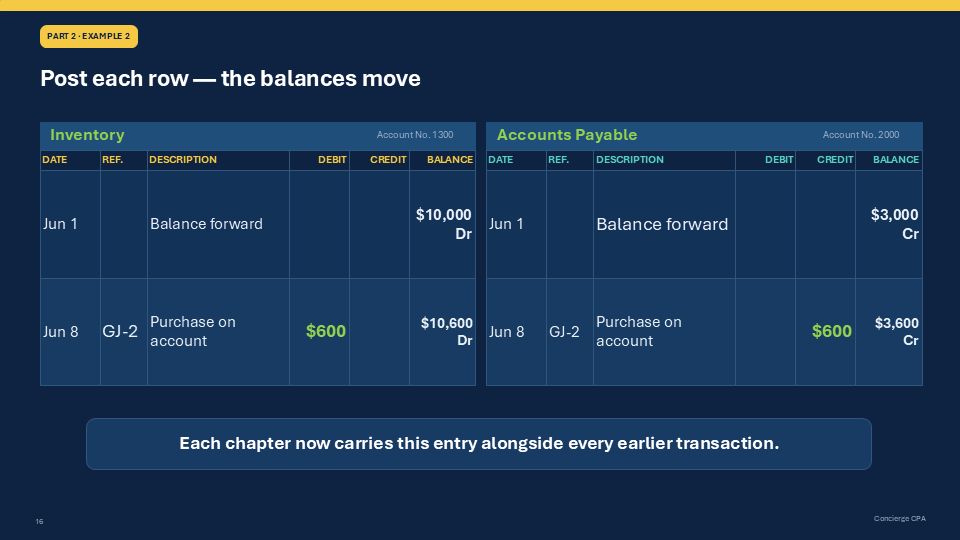

Example 2: Posting an Inventory Purchase on Account

Now assume the business buys $600 of inventory from a supplier and agrees to pay later.

The journal entry would be:

- Debit inventory for $600

- Credit accounts payable for $600

Here is how that moves through the general ledger.

Inventory

The $600 debit is posted to the inventory account.

If inventory already had a debit balance of $10,000, posting the new amount brings the balance to $10,600.

Accounts Payable

The $600 credit is posted to the accounts payable account.

If accounts payable already had a credit balance of $3,000, the posting raises it to $3,600, just as you would see when recording notes payable journal entries and updating loan-related balances.

Again, each line of the journal entry goes to its own place in the general ledger. The inventory account now reflects the new purchase along with all previous inventory activity, and the accounts payable account reflects the new obligation along with all other unpaid amounts.

What Posting Looks Like in T Accounts

T accounts are the classic way to visualize ledger accounts, and they make posting easy to see. Each account is drawn as a large T, with the account name across the top, a debit column on the left, and a credit column on the right.

When you post, debit entries go into the left column of the affected account, and credit amounts go into the right column. The account balance is simply the difference between total debits and total credits in that account, which is why understanding debits and credits in accounting is so important.

Take Example 1. The accounts receivable T account starts with $4,000 in the debit column. The new $1,000 debit is posted beneath it, bringing the balance to $5,000 on the debit side. Meanwhile, the service revenue T account shows $8,000 in the credit column, and the new $1,000 credit brings that balance to $9,000.

T accounts are a teaching tool more than a real-world format, but they capture exactly what the general ledger does: each account collects its own debits and credits and carries a balance.

How the General Ledger Keeps Running Balances

One of the most important jobs of general ledger posting is maintaining a running balance for every account. You never have to manually calculate account balances from scratch — every posting updates the balance automatically, whether the system does it or you do it by hand.

As more transactions are posted:

- The cash account keeps tracking every dollar received and paid out

- Accounts receivable keeps accumulating customer balances owed

- Inventory keeps accumulating purchases and other inventory activity

- Accounts payable keeps accumulating amounts owed to suppliers

- Revenue and expense accounts keep building the activity for the period

The same logic applies to every account type — assets, liabilities, equity, revenue, and expenses, all of which follow the 3 Golden Rules of Accounting in a double-entry system. This running balance is what makes the ledger useful. It does not just list activity. It shows where each account stands after every posting.

From Paper Books to Accounting Software

Businesses no longer maintain giant leather-bound books for most accounting systems, but the old terminology has stayed with us. Accountants still talk about ledgers, bookkeeping, posting entries, and closing the books.

That language survives because the structure still works the same way. Modern software simply turns the general ledger into a digital database, but the underlying financial accounting principles and reporting remain the same.

Instead of flipping to a paper chapter for accounts receivable, you open the account on a screen. Instead of writing in a ledger by hand, the system posts the entry electronically — usually the instant you save the journal entry. But the purpose remains identical: organize all financial activity by account and maintain accurate balances.

Why Posting to the General Ledger Matters

If the general ledger only stored transactions, it would already be useful. But it matters for a much bigger reason. It becomes the foundation for the rest of the accounting cycle.

At the end of an accounting period, accountants do not stop with the posted transactions. They also move through the remaining steps of the broader accounting cycle. They also:

- Record adjusting journal entries

- Review account activity

- Reconcile balances

- Confirm that balances are supported by documentation

That process helps ensure the accounts are complete and accurate. It is also how accountants verify the records and catch errors — a line posted to the wrong account, a missed entry, or a balance that does not agree with its support.

Once routine transactions are posted to the general ledger, some accounts still need adjustment. That is where adjusting journal entries come in, followed later by closing entries that reset temporary accounts. These entries bring the records up to date at the end of the period.

After that, the balances in the general ledger are reviewed and reconciled. Reconciliation means checking that the balance shown in the account agrees with the underlying support. That support may include transaction details, schedules, or other valid documentation.

Together, the journal entries, account activity, reconciliations, and supporting records create a clear trail showing how each ending balance was built. This is what gives the accounting records reliability. The general ledger is not just a storage tool. It is part of the evidence behind the company’s numbers.

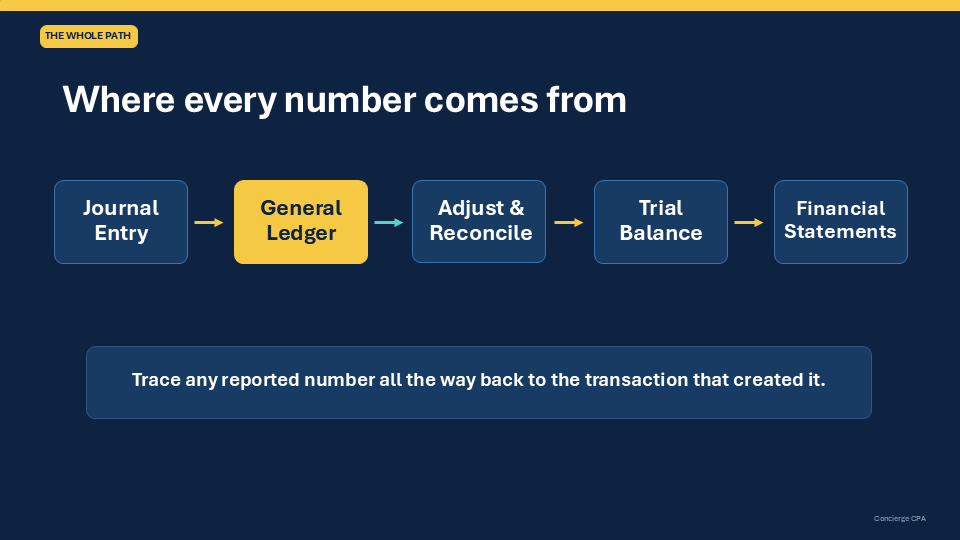

From the General Ledger to the Trial Balance and Financial Statements

Once the accounts have been posted, adjusted, and reconciled, the ending balances from the general ledger are gathered into the trial balance. The trial balance lists every general ledger account with its ending balance and confirms that total debits equal total credits across all accounts.

From there, the financial statements are prepared. The balance sheet shows the assets, liabilities, and equity balances. The income statement shows the revenue and expense activity for the period. Those same ledger balances also support tax filings and other reporting the business has to produce.

That flow looks like this:

- Journal entries are recorded

- Each line is posted to the general ledger account it affects

- Accounts are adjusted as needed

- Balances are reconciled and supported

- Ending balances are collected in the trial balance

- Financial statements are prepared from the trial balance

So when you see a balance on the financial statements, it did not appear out of nowhere. It traces back through the trial balance to the general ledger, and from there back to the underlying journal entries and support.

FAQ

What is the difference between a journal and a general ledger?

The general journal records complete transactions in chronological order — each entry shows the full debit and credit together, on the date it occurred. The general ledger organizes those same lines by account, with each account keeping a running balance. Transactions are recorded in the journal first, then posted to the ledger.

What is the difference between the general ledger and subsidiary ledgers?

The general ledger holds the control accounts, such as total accounts receivable. A subsidiary ledger breaks a control account into detail — for example, the individual balance owed by each customer. The detail in a subsidiary ledger must always agree with its general ledger control account.

What does “post to the ledger” mean in accounting?

It means transferring each line of a journal entry into the correct general ledger account so the account balances stay current. Each debit and credit is placed into the account it affects, and that account’s running balance is updated.

Final Takeaway

Posting to the general ledger is how individual transactions become organized, usable account balances. Each line of a journal entry is transferred into the account it affects, where it joins that account’s history and updates the running balance. From there, the balances are adjusted, reconciled, gathered into the trial balance, and used to prepare the financial statements.

Once that clicks, posting is no longer a vague textbook phrase. It is a specific and essential step in how accounting data moves from individual transactions to meaningful financial reports.