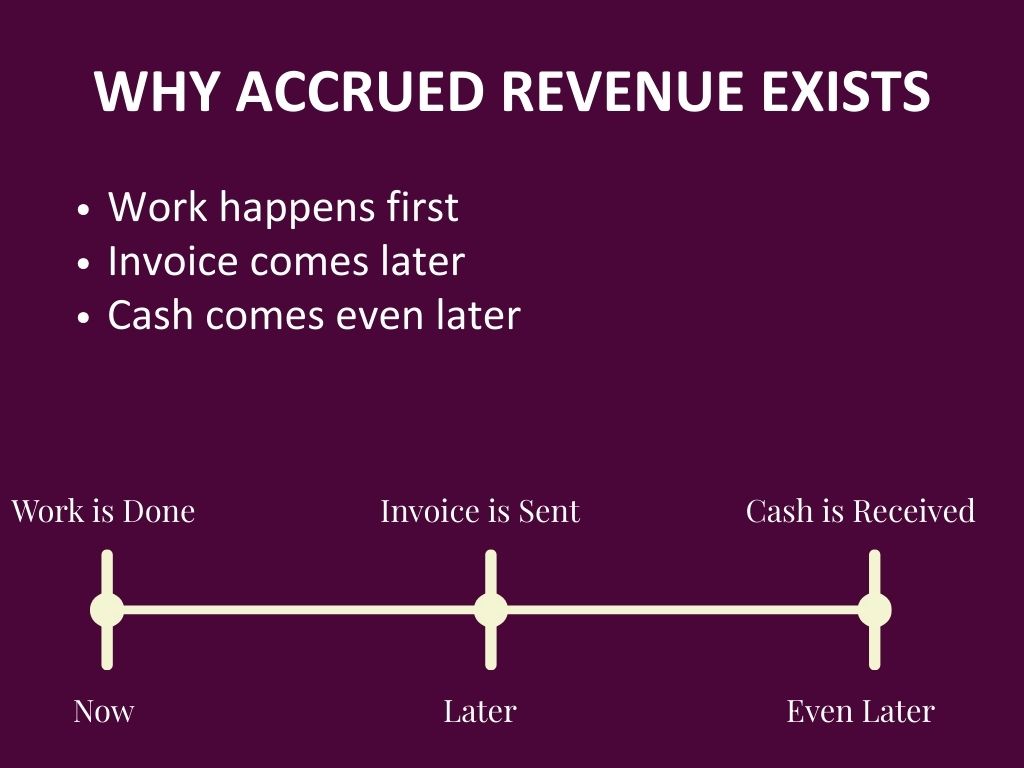

Accrued revenue is revenue a company has earned but has not yet billed or received as a cash payment. Under the accrual accounting method, revenue is recognized when performance obligations are satisfied—not when the customer pays. That timing difference often makes businesses look profitable on the income statement while cash flow remains tight. This guide explains what accrued revenue is, how to record accrued revenue, when to classify it as current or noncurrent, common pitfalls, and practical month-end procedures for accurate financial reporting.

What Is Accrued Revenue?

Accrued revenue (also called unbilled receivable, accrued income, or contract asset) arises when a company delivers goods or services and has a right to receive payment, but no invoice has been issued and cash has not been collected.

The accrued revenue criteria include:

- Revenue has been earned—performance obligations under the contract are met

- No invoice has been sent (unbilled) or the invoice has not yet been paid

- The company expects to collect cash in the future and records an asset to reflect that right

Accrued revenue is an asset because the company has a legal right to receive payment for work already performed.

Why Is Accrued Revenue Important?

The accrual accounting process seeks to match income to the accounting period when economic activity occurs. The revenue recognition principle under ASC 606 and generally accepted accounting principles (GAAP) requires recognizing revenue when the company satisfies its performance obligations—when the customer receives the promised benefit—rather than when cash receipts arrive.

Recording accrued revenue ensures financial statements reflect the true timing of business activity. Without proper revenue recognition, a company’s financial performance would be misstated, and the income statement reflects an inaccurate picture of earned revenue.

Accrued revenue serves a critical function: it aligns reported income with actual work completed, ensuring accurate financial reporting and supporting proper revenue recognition throughout the revenue recognition process.

How to Record Accrued Revenue: Journal Entries and Flow

Recording accrued revenue typically involves three stages: the adjusting journal entry at period end, converting the accrual into a normal receivable when invoiced, and collecting cash.

Adjusting Entry When Work Is Done but Not Billed

Account | Credit | |

|---|---|---|

Contract Asset (Accrued Revenue) | $X | |

Service Revenue (Income Statement) | $X |

When Invoice Is Issued

Account | Debit | Credit |

|---|---|---|

Accounts Receivable and Notes Payable Journal Entries | $X | |

Contract Asset (Accrued Revenue) | $X |

When Customer Pays

Account | Debit | Credit |

|---|---|---|

Cash | $X | |

Accounts Receivable | $X |

Important: revenue is recognized once—when earned. Subsequent entries only reclassify the asset from contract asset to accounts receivable account to cash. Recording revenue again at billing or when the customer pays would overstate income.

Example of Accrued Revenue: Consulting Firm Completes Project

Scenario: A consulting firm completes a $12,000 project on December 31. Invoice is sent January 10. Client pays January 25.

December 31 (adjusting entry): Debit contract asset $12,000; Credit service revenue $12,000. The income statement reflects $12,000 revenue for December within the same accounting period the work was performed.

January 10 (billing): Debit accounts receivable $12,000; Credit contract asset $12,000. No additional revenue recorded.

January 25 (collection): Debit cash $12,000; Credit accounts receivable $12,000.

Result: December income reflects the work done even though cash payment arrived in January. The financial statements reflect economic reality, not just cash transactions.

Contract Asset vs Accounts Receivable

Under ASC 606, the term contract asset is commonly used for accrued revenue when the company has performed but billing is conditional or delayed. The accounts receivable account is used once the entity has invoiced and the right to payment is unconditional. This presentation matters for working capital and covenant calculations on the balance sheet.

Is Accrued Revenue a Current Asset?

Classify accrued revenue as a current asset or noncurrent asset based on expected collection timing:

Current asset: Billing and collection expected within 12 months or the operating cycle. This is when accrued revenue occurs most frequently.

Noncurrent asset: Billing or collection expected beyond 12 months. Typical in long-term construction company contracts, milestone payments, or deferred billing arrangements.

Industries Where Accrued Revenue Occurs

Accrued revenue accounting is common in:

- Professional services (consulting firm, accountants, lawyers)

- Software as a service and tech companies (usage-based or milestone billing)

- Construction company and engineering firms (long-term contracts with milestone or retention payments)

- Contracted project work (web development, advertising agencies)

- Accrued interest income or interest revenue where payment timing lags performance

How Accrued Revenue Affects Financial Statements and Cash Flow

Accrued revenue increases reported revenue and net income without an immediate cash effect. Understanding this impact is essential for managing accrued revenue and evaluating a company’s financial health:

- Financial performance measures (gross margin, operating profit) may look strong while cash flow remains weak

- The balance sheet can be overstated if unbilled receivables are recorded but collection risk is high

- Cash planning must rely on accounts receivable aging and contract terms rather than income alone—you must manage cash flow separately from reported earnings

- Bank covenants and metrics tied to EBITDA may improve on paper even if liquidity is constrained

The matching principle ensures expenses and revenue are recorded in the same accounting period, but this doesn’t guarantee cash receipts align with recognizing revenue.

Month-End Checklist for Managing Accrued Revenue

- Identify completed performance obligations using contract terms and deliverables

- Calculate amounts to accrue based on contracts, time records, percent complete, or milestones

- Prepare the adjusting journal entry to debit contract asset and credit the revenue account

- Document support (contracts, completion memos, acceptance emails) to justify when revenue is recognized

- Reconcile contract assets to billing schedules and subsequent invoices

- Classify current vs noncurrent based on agreed billing and payment timing

- Review collectibility—if payment is not probable, do not recognize accrued revenue; consider allowances

This process supports ensuring accurate financial reporting and proper revenue recognition.

Common Mistakes When Recording Accrued Revenue

Double-counting revenue: Recording revenue on both the adjusting entry and when invoicing. Avoid by only recognizing revenue when earned.

Ignoring contract terms: Revenue recognition must follow the contract—billing schedule, acceptance criteria, and performance obligations determine when does accrued revenue get recorded.

Misclassifying assets: Treat contract assets separately from accounts receivable accrued revenue until the invoice creates an unconditional right.

Overlooking collectibility: If payment is not probable, revenue recognition may be inappropriate under ASC 606.

Incorrect cutoff: Failing to record accrued revenue for work completed before period end leads to misstated income. The income statement reflects only what’s recorded.

Accrued Revenue vs Deferred Revenue

Accrued revenue and deferred revenue (also called unearned revenue) are timing opposites:

Accrued Revenue | Deferred Revenue | |

|---|---|---|

Timing | Revenue recognized before cash payment | Cash received before revenue is recognized |

Balance Sheet | Asset (right to receive payment) | Liability (obligation to deliver goods or services) |

Also Called | Unbilled revenue, accrued income, contract asset | Unearned revenue, contract liability |

Deferred and accrued revenue both result from timing differences between cash transactions and when revenue is recognized, but they appear in different sections of the balance sheet.

With accrued revenue vs deferred revenue, the key question is: Did you perform work first (accrued) or receive payment first (deferred)?

Examples of Accrued Revenue: Which of the Following Qualifies?

A consulting firm completes work in March, bills in April: This is accrued revenue. The firm must record revenue in March when the performance obligation was satisfied, then record accrued revenue as an asset until the customer pays.

A software as a service company receives annual payment upfront: This is deferred revenue (unearned revenue), not accrued revenue. Cash came first; the revenue account is credited as services are delivered each month.

A construction company finishes a milestone but contract delays billing: Accrued revenue. The company has earned revenue and should recognize accrued revenue even though billing is delayed.

Accrued interest income on a loan: Accrued revenue. Interest revenue is earned with the passage of time, so interest income must be recorded even before the customer pays.

Accrued Revenue vs Accrued Expense

While accrued revenue represents earned revenue not yet billed, an accrued expense represents costs incurred but not yet paid. Both are adjusting entries required under the accrual accounting method:

- Accrued revenue = asset (you’re owed money)

- Accrued expense = liability (you owe money)

Both ensure financial statements reflect economic reality within the correct accounting period.

Key Takeaways: Accrued Revenue

- Accrued revenue reflects earned revenue before billing or cash receipts

- Revenue is recognized when performance obligations are satisfied under ASC 606 and the revenue recognition principle

- Record an adjusting entry to create a contract asset and credit the revenue account; later reclassify to accounts receivable when invoiced

- Monitor collectibility and contract terms—these determine whether and when to recognize accrued revenue

- Accrued revenue is an asset; deferred revenue (unearned revenue) is a liability

- Proper accrued revenue accounting supports accurate financial reporting and helps stakeholders assess a business’s financial health and company’s financial performance

Properly recording accrued revenue aligns reported income with economic activity and supports ensuring accurate financial reporting. This gives stakeholders a true picture of financial performance and helps manage cash flow expectations appropriately.

For a visual walkthrough of accrued revenue journal entries and examples, watch my video on the MyConcierge CPAYouTube channel.