If you’re learning accounting, the trial balance can feel like one more report to memorize. It makes a lot more sense once you see where it comes from.

Journal entries, the general ledger, and the trial balance aren’t separate topics. They’re one connected system, and together they form the backbone of the accounting cycle. Every transaction starts as a journal entry, gets organized in the ledger, and lands in the trial balance before any financial statements are prepared.

After 25 years of corporate accounting close work, I can tell you the trial balance you learn in school is only half of what actually happens in practice. Most beginner lessons stop at the textbook trial balance. But in real corporate close work, there’s a step beyond that almost no tutorial covers: the trial balance bridge. It’s what accountants actually build when post-close adjustments come in after the original trial balance has already gone out to auditors.

We’ll walk through the full flow first, then cover the three types of trial balance you’ll see in practice, and finish with what the bridge looks like and why it matters.

The flow: journal → ledger → trial balance

Every business records financial activity the same way, whether it’s a freelancer or a Fortune 500. The accounting cycle has three foundational stages before financial statements get prepared.

Journal entries are where transactions are first recorded. A sale, an expense, a loan, an owner contribution. Every entry has a debit and a credit, and the two sides have to be equal. That’s the foundation of double-entry bookkeeping.

The general ledger takes those journal entries and reorganizes them by account, using the company’s chart of accounts as the master list. If the journal is your inbox, the ledger is your filing cabinet. Instead of digging through every entry to figure out your cash position, you go straight to the cash account and see everything that hit it. Each account in the general ledger carries its own running balance.

The trial balance pulls all of those ledger account balances into one report. It’s a snapshot at a single point in time, and its main job is to confirm that total debits equal total credits before you start preparing financial statements. That’s why it’s called a trial balance — you’re testing whether the books balance.

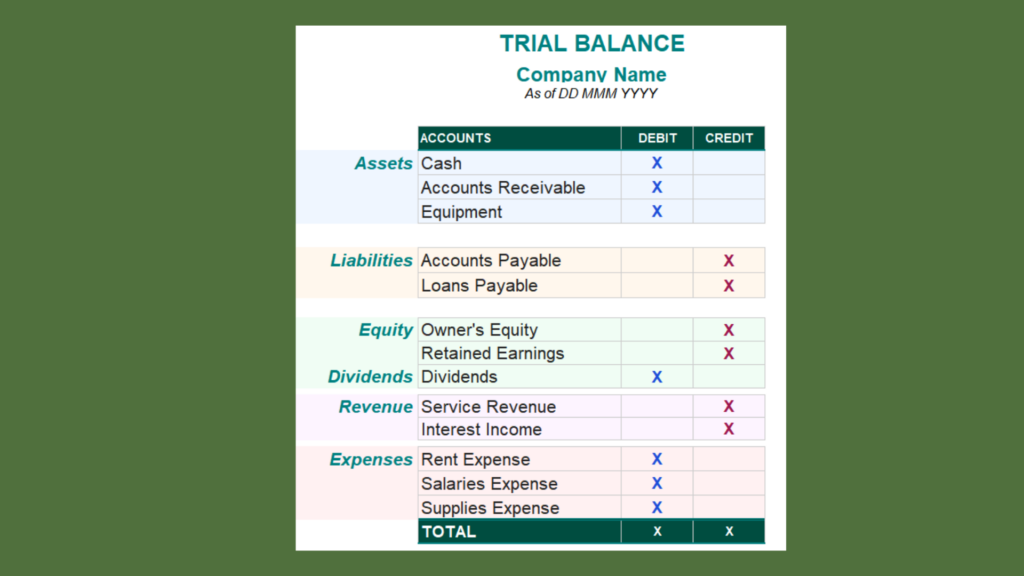

Trial Balance Format

The header carries three things: company name, the report title (Trial Balance), and the date. Always a specific date, never a date range. A trial balance is a snapshot, not a period summary.

The body has three columns: account name, debit balance, and credit balance. Each account shows up once, and its balance lands in only one column based on its normal balance. Asset and expense accounts run debit. Liability, equity, and revenue accounts run credit, following the basic rules for debits and credits in accounting. Zero-balance accounts are usually left off to keep the report clean.

Accounts are listed in a standard order that mirrors the chart of accounts and the accounting equation:

- Assets

- Liabilities

- Equity

- Dividends

- Revenue

- Expenses

That same sequence carries through to the balance sheet and income statement, so following it now makes financial statement preparation easier later.

At the bottom, the debit column and credit column are totaled. If they don’t match, you have an error somewhere — a posting in the wrong column, a one-sided entry, or a math mistake.

A note on the working trial balance format

There’s a second format you’ll see all the time in practice. A working trial balance uses a single amount column instead of two. Debits are positive numbers. Credits are negative, usually shown in parentheses. When everything is posted correctly, the whole column totals to zero.

This is the format most accountants default to in Excel, because it’s faster to analyze, easier to compare across accounting periods, and much easier to layer adjustments onto. We’ll come back to it in the bridge section.

Trial Balance Examples: Four Transactions

The cleanest way to see the flow is to trace a few transactions all the way through. We’ll set up a simple consulting business.

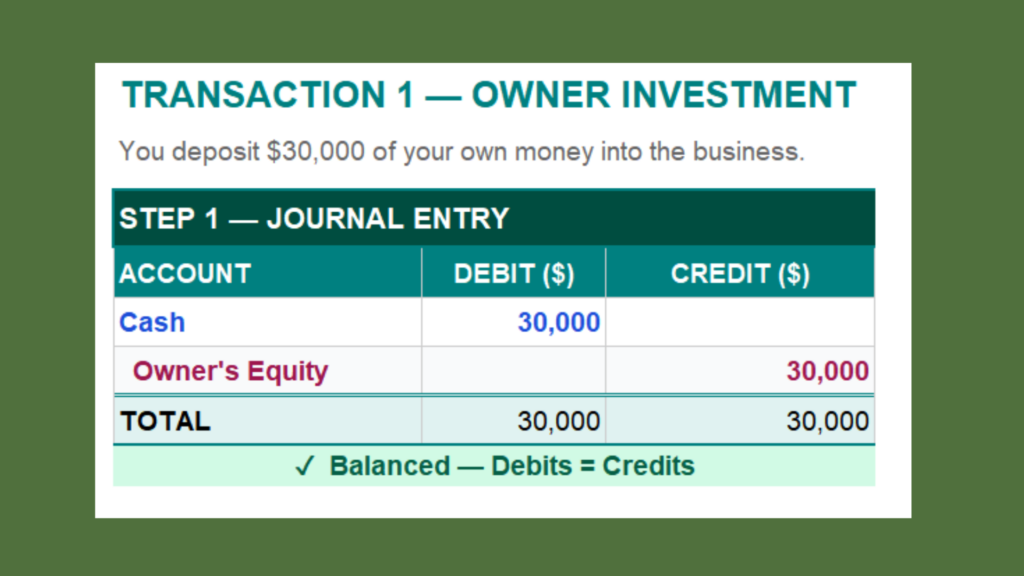

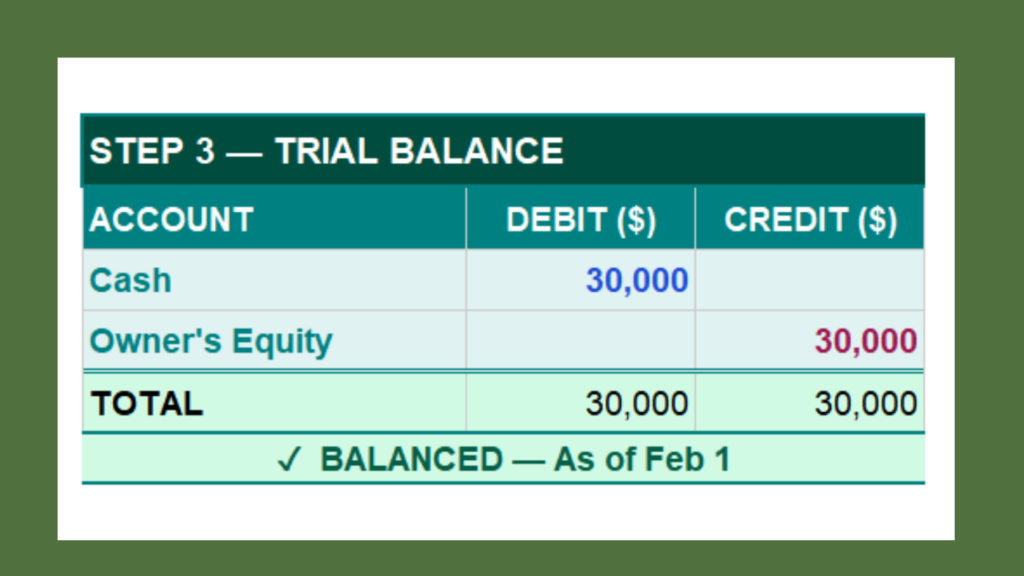

Transaction 1: Owner invests $30,000 cash.

Journal entry: Debit Cash $30,000, Credit Owner’s Equity $30,000. Cash is an asset (increases with a debit). Owner’s equity increases with a credit, consistent with the golden rules of accounting.

After posting to the ledger, the trial balance shows:

- Cash: $30,000 Dr

- Owner’s Equity: $30,000 Cr

Debits equal credits. Balanced.

Transaction 2: Buy equipment for $8,000 on account.

Journal entry: Debit Equipment $8,000, Credit Accounts Payable $8,000.

The trial balance now shows:

- Cash: $30,000 Dr

- Equipment: $8,000 Dr

- Accounts Payable: $8,000 Cr

- Owner’s Equity: $30,000 Cr

Totals: $38,000 on each side.

Transaction 3: Complete a client project and receive $6,000 cash.

Journal entry: Debit Cash $6,000, Credit Service Revenue $6,000.

Transaction 4: Pay $1,500 rent.

Journal entry: Debit Rent Expense $1,500, Credit Cash $1,500.

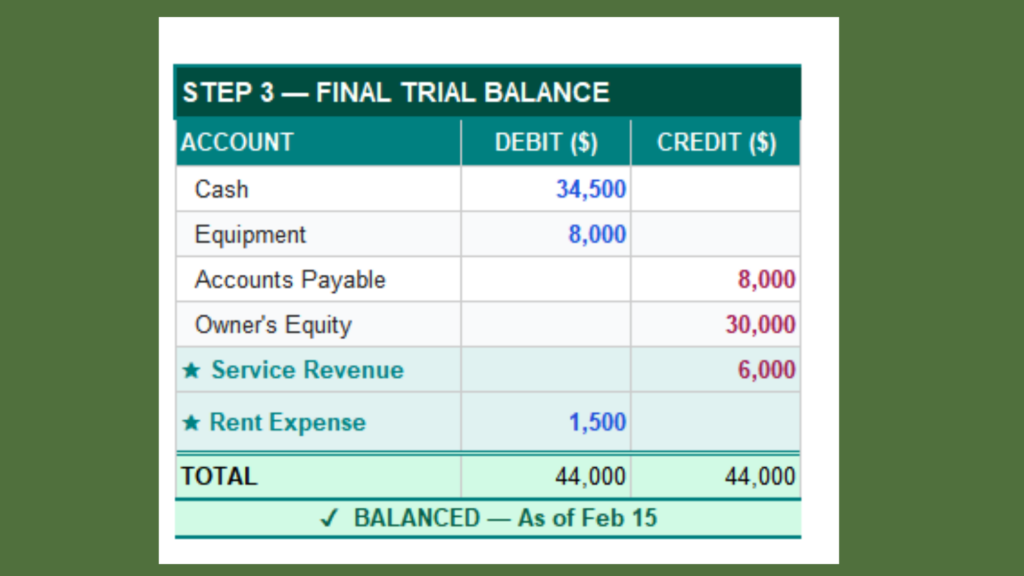

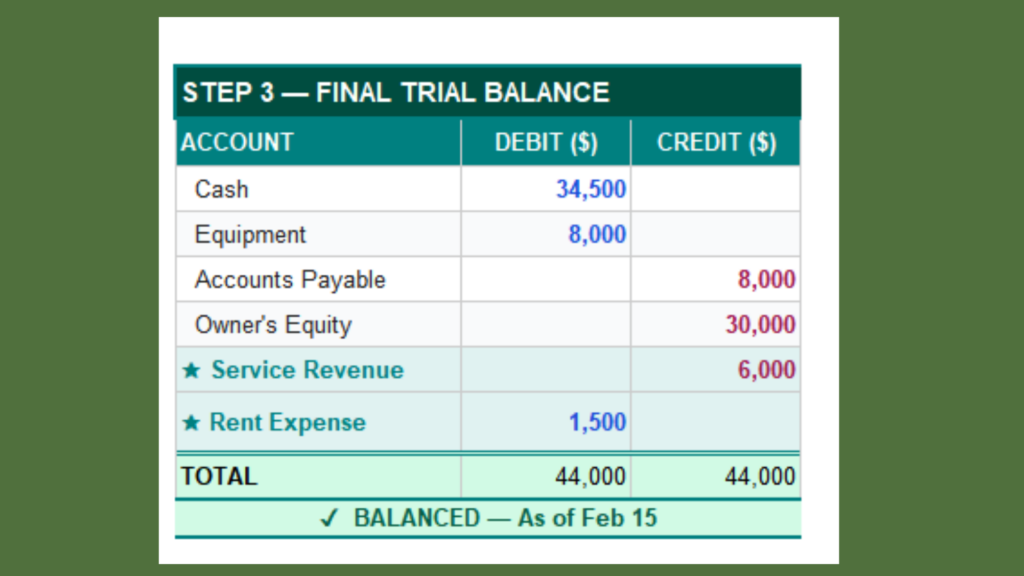

After all four transactions, the cash account has been hit three times: +$30,000, +$6,000, -$1,500. That leaves a $34,500 balance. The full trial balance:

- Cash: $34,500 Dr

- Equipment: $8,000 Dr

- Accounts Payable: $8,000 Cr

- Owner’s Equity: $30,000 Cr

- Service Revenue: $6,000 Cr

- Rent Expense: $1,500 Dr

Totals: $44,000 on each side.

The point is that every one of those transactions traveled the same path through the accounting cycle. Journal → ledger → trial balance. Nothing skipped a step.

Why this still matters when software does the work

QuickBooks, NetSuite, Sage, and every other accounting platform can produce a trial balance on demand. The mechanics underneath aren’t optional knowledge, though, because they sit inside the broader framework of financial accounting.

A balanced trial balance only proves one thing: total debits equal total credits. It doesn’t prove anything was recorded in the right account. An amount could be posted to the wrong expense line. A transaction could be missed entirely. A reclassification could still be sitting on your desk. Balanced is not the same as correct.

If you can’t read a trial balance and understand how each balance was built, you can’t spot those errors. You also can’t explain balances to your manager, your auditor, or on an exam. Accounting software is a calculator, not a substitute for understanding.

The three types of trial balance

Before getting to the bridge, it helps to know there are three versions of the trial balance you’ll see across an accounting period, each prepared at a different stage of the close.

Unadjusted trial balance. The first version, pulled after all transactions for the period have been posted to the general ledger but before any adjusting entries. It’s the starting point for the close.

Adjusted trial balance. The version after adjusting entries are recorded — accruals, deferrals, depreciation, prepaid amortization. This is the trial balance that gets used to prepare the balance sheet and income statement.

Post-closing trial balance. The version after closing entries have moved revenue, expense, and dividend balances into retained earnings. Only permanent (balance sheet) accounts remain, and the totals carry forward as the opening balances for the next accounting period.

The trial balance bridge lives between the unadjusted and adjusted versions, but with a twist most courses don’t cover.

The trial balance bridge: what beginner courses skip

Here’s where things get practical.

In a real corporate close, the accounting team finishes the period, prepares the trial balance, and sends it to auditors, the tax team, or both. That’s the original trial balance for the period — often before every adjustment has been finalized.

But accounting doesn’t stop the moment that file goes out. The team almost always identifies items afterward:

- A missed accrual

- Revenue recognized in the wrong period

- A reclassification an auditor flags

- An expense that should have been recognized before close

Now there’s a gap between the trial balance that was sent out and the final adjusted trial balance in the books. Somebody — usually you — has to document exactly how you got from one to the other. That’s what the bridge does.

What Is a Trial Balance Bridge?

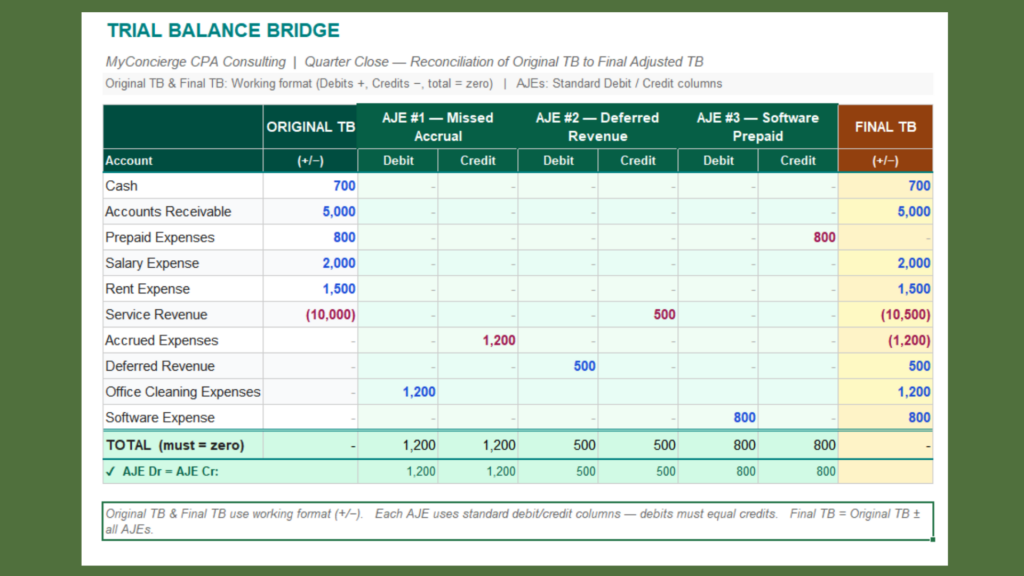

A trial balance bridge is a manually built Excel schedule that connects the original trial balance to the final adjusted trial balance, one adjustment at a time. It doesn’t come out of any accounting software automatically. You build it by hand.

The structure is straightforward. Start with the original working trial balance on the left. Add a column (or set of columns) for each adjusting journal entry. End with the final adjusted trial balance on the right.

Every adjustment is still a journal entry, so every adjustment column has to balance to zero on its own. Not just the final total — each adjustment, on its own, must have debits equal to credits.

The result is a clean left-to-right story of exactly what changed and why.

Trial Balance Example With Adjusting Entries

Say the original trial balance has already been sent out at quarter-end close. Three adjustments come up afterward.

Adjustment 1: Missed accrual for office cleaning services.

Services were performed before period-end but not yet invoiced.

- Debit Office Cleaning Expense $1,200

- Credit Accrued Expenses $1,200

The expense increases, and the liability increases.

Adjustment 2: Deferred revenue recognition.

Cash received the prior quarter was recorded as deferred revenue. The service was performed this period, but the recognition entry didn’t make it in before the trial balance went out.

- Debit Deferred Revenue $500

- Credit Service Revenue $500

The liability goes down, and revenue goes up.

Adjustment 3: Prepaid software amortization.

A quarterly software subscription was paid up front and recorded as prepaid expense. The used portion wasn’t moved to expense before close.

- Debit Software Expense $800

- Credit Prepaid Expenses $800

The asset decreases, and the expense increases.

In the working trial balance format, those adjustments lay across the sheet as three separate columns. Each column nets to zero. The final column on the right is the adjusted trial balance: the original numbers plus or minus each adjustment, line by line.

Why it’s more than a reconciliation

A bridge isn’t just a reconciliation. It’s a communication tool. Anyone reviewing the file — auditor, tax preparer, controller, or CFO — can trace the entire story from the original trial balance to the adjusted trial balance without a single follow-up question. They see what you sent, what you found after, and where you ended up.

Anyone who’s spent time on a close team has fielded a version of “why did this number change between the file you sent us Tuesday and the file we got Friday?” The bridge exists to answer that question before it ever gets asked. It saves hours of email back-and-forth and protects the close team from looking sloppy.

Key rules to remember

- A trial balance is a point-in-time report. Always use a single date.

- Each account appears once, in either the debit or credit column, never both.

- Zero-balance accounts are usually omitted.

- Standard order: assets, liabilities, equity, dividends, revenue, expenses.

- Total debits must equal total credits.

- A balanced trial balance is not proof of accuracy. Review still matters.

- A working trial balance uses one column. Debits positive, credits negative, total equals zero.

- The three types: unadjusted, adjusted, and post-closing trial balance, each at a different stage of the accounting cycle.

- A trial balance bridge is built by hand. Every adjustment must balance on its own.

The bigger picture

Once the flow clicks, the pieces stop feeling random.

The journal entry is where a transaction is born. The general ledger organizes those entries by account. The trial balance gathers the balances and tests them before the balance sheet and income statement are prepared. And in real close work, the trial balance bridge is what shows your work after the original trial balance has already been sent out.

That last piece is what turns the trial balance from a textbook exercise into how the accounting work actually gets done.